Captive Insurance

Turning Insurance into a financial asset!

Are you tired of subsidizing other business’ claims?

Captive Insurance may be for you.

As insurance costs continue to rise and coverage becomes more restrictive, many businesses are exploring alternative ways to manage risk. Captive insurance can offer qualified organizations greater control, long-term cost stability and customized risk management strategies.

common questions

-

A captive is an insurance company you own. Instead of paying premiums to a traditional carrier and never seeing that money again, your business (often alongside other like-minded companies) funds a captive that insures your risk. You keep control of the dollars, and when claims stay low, the savings come back to you instead of staying with the carrier.

-

With traditional insurance, you pay a premium, the carrier keeps the profit, and good loss years benefit them, not you. With a captive, you share in the underwriting profit and investment income. Traditional pricing is driven by the broader market. Captive pricing is driven by your own performance. The tradeoff: a captive requires more commitment, a stronger balance sheet, and a genuine focus on controlling losses.

-

You still pay premiums, but they flow into your captive rather than disappearing into a carrier's pool. Those dollars cover your claims and operating costs. Whatever is left at the end of the year stays in the captive as surplus, and that surplus earns interest while it sits there. Over time, the combination of retained premium and investment income builds into real, accessible value tied to how well you manage risk.

-

In the traditional model, your premium is gone the moment you pay it. In a captive, that premium funds a company you have an ownership stake in. If your losses come in lower than expected, the difference belongs to you and the other owners, not the carrier. You are still paying for protection, but you are also building equity in the process.

-

Captives fit financially strong businesses that take risk seriously. The general benchmark is $150,000 or more in annual premium across your liability coverages (Workers' Compensation, Auto Liability, and General Liability), but premium size is only the starting filter. The best candidates also bring a strong balance sheet, a real dedication to loss control and safety, and a good loss history. If that's you, a captive flips insurance on its head, turning it from a liability you write checks against into an asset you build value in.

-

Back to you, as the business owner.

In the standard market, the premium you don't use becomes the insurance company's profit. In a group captive, it becomes yours. Your premium is split into pieces: a portion funds your expected claims, a portion covers shared risk with the other members, and a portion pays operating costs. When your claims come in lower than what was funded, the unused money is returned to you as a dividend, along with the investment income it earned.

Two honest caveats. Dividends are earned, not guaranteed. They reflect how well you and your fellow members manage risk. They also take time, since claim years have to mature and close before funds are released. Distributions typically begin a few years into membership and continue year over year after that. Captive members think in decades, not renewal cycles.

For companies with strong safety cultures, this is the difference between insurance you buy and insurance you own. The protection is the same. The ownership is what pays you back.

Still have questions?

Why should a business consider captive insurance?

Greater Control

Potential Cost Stability

Improved Risk Awareness

Financial Advantages

Access to Special Coverage

How a captive is structured

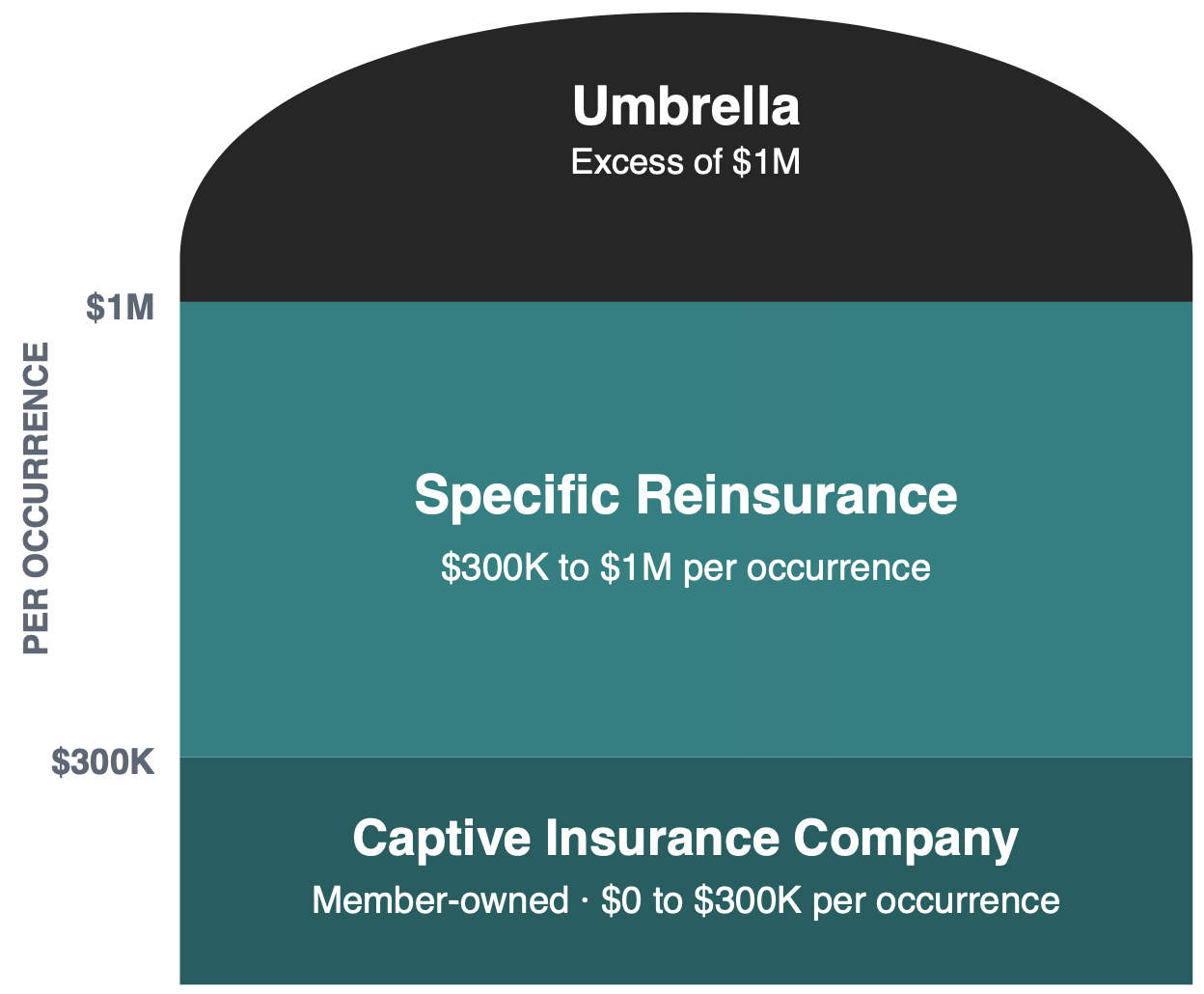

Maximum reward, controlled risk

A well-designed captive doesn't ask members to swallow unlimited risk. The program is engineered in layers. Predictable losses are funded inside the captive, catastrophic losses transferred to reinsurance, and tower limits handled by traditional umbrella. Each layer is sized to the member's appetite and the family's balance sheet.

Umbrella

Purchased outside the captive for additional tower limits above the $1M attachment.

Specific Reinsurance

The captive buys reinsurance to protect against any single loss above the member retention.

captive layer

Each member funds and is responsible for claims inside this layer (e.g., $0 to $300K). Profitable years return to members.

Ford's Risk-Sharing Commitment

Captive ownership is a partnership, and a long one. Ford and our captive program partners stay aligned with our members on program performance. Through transparency, consistent engagement, and a Northern Michigan relationship that doesn't turn over every 18 months, we stay accountable for outcomes year after year, not just at inception.

What types of businesses are good candidates?

Most businesses with significant insurance premiums are possible candidates for using captive insurance. Companies with strong cultures centered around safety and predictable claims histories should also explore captive insurance strategies.

Multi location Businesses

Manufacturing

Construction

Healthcare

Municipalities

Hospitality

Agriculture

hotels & Motels

It’s time to meet josh!

Are you facing rising premiums? Sick of last-minute renewal proposals? Looking for an agent familiar with business insurance?

Josh Hart supports Michigan businesses of all sizes and specialties in our region. He’d be happy to help! You can call him directly at (231) 221-2707 or email him at jhart@fordinsurance.net.

CALL: (231) 221-2707

EMAIL: jhart@fordinsurance.net

Or if you’d prefer, click below to fill out a form and he will get back to you.